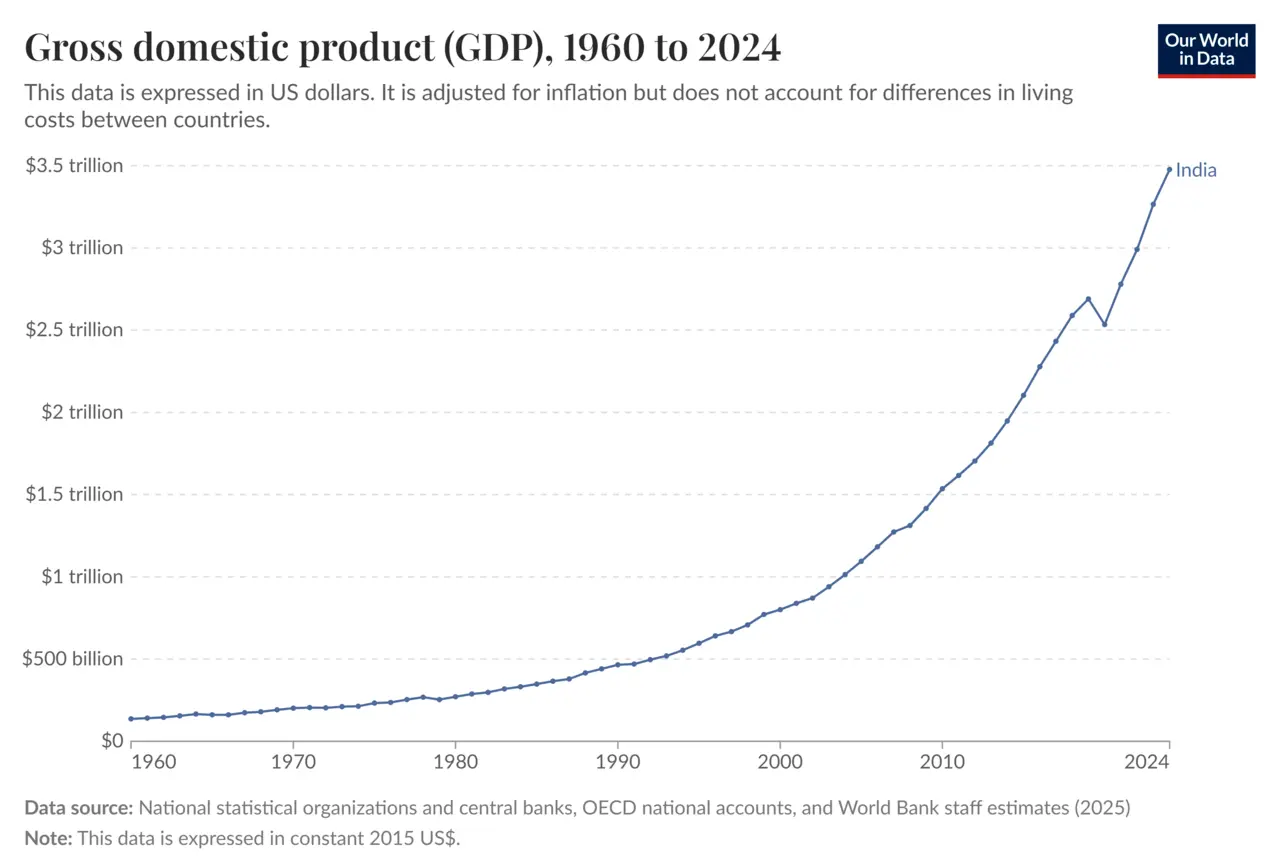

India’s recent movement from the fourth to the sixth largest economy in certain global rankings has triggered commentary, concern, and in some quarters, misplaced pessimism. At face value, such a shift appears to signal an erosion of economic strength. However, this interpretation risks oversimplifying a far more complex reality. In my view, this development is less an indication of economic decline and more a reflection of the limitations embedded in global measurement systems—particularly rankings based on nominal GDP in US dollar terms.

The most immediate factor behind this apparent decline is the depreciation of the Indian rupee. India’s economy has not contracted; in fact, it continues to expand at one of the fastest rates among major economies. Yet, because global rankings convert national output into US dollars, even moderate currency depreciation can significantly compress the perceived size of the economy.

This creates a peculiar paradox: growth on the ground coexists with a decline in global position. Alongside currency effects, revisions in GDP methodology, changes in base year calculations, and periodic data recalibrations have further influenced economic estimates, adding technical distortions to what is often interpreted as a structural weakening.

However, attributing this entirely to domestic policy would be analytically incomplete. The rupee’s movement is deeply shaped by global financial and geopolitical conditions.

India imports nearly 85% of its crude oil requirements, making it particularly exposed to external energy shocks. Geopolitical instability in major oil-producing regions elevates import costs, widens the trade deficit, and increases demand for dollars, thereby exerting pressure on the rupee.

At the same time, tighter monetary conditions in advanced economies—particularly elevated interest rates in the United States—have strengthened the dollar globally, triggering portfolio outflows from emerging markets such as India. In this environment, currency depreciation is not a uniquely Indian problem; it is part of a broader global financial realignment.

From a domestic standpoint, the implications of this ranking shift are nuanced rather than uniformly negative.

A weaker rupee undoubtedly raises import costs, contributes to inflationary pressures, and can temporarily affect investor sentiment. However, it also improves export competitiveness by making Indian goods and services relatively cheaper in international markets. Sectors such as IT services, pharmaceuticals, textiles, and manufacturing can benefit from this currency adjustment.

The real issue, therefore, is not the ranking itself but what it reveals about India’s external vulnerabilities—particularly dependence on imported energy and exposure to volatile capital flows.

A crucial dimension often overlooked in headline discussions is that India’s underlying growth momentum remains strong.

Recent projections from the United Nations indicate that India is expected to remain one of the fastest-growing large economies globally, with growth projections in the range of approximately 6.2–6.5%, significantly outperforming most advanced economies and several major emerging markets. While growth in much of Europe remains subdued and global expansion faces persistent uncertainty, India continues to be supported by strong domestic demand, infrastructure spending, digital transformation, and favourable demographics.

This reinforces an important point: nominal GDP rankings are heavily influenced by valuation effects and do not always reflect real economic dynamism.

Indeed, India’s long-term structural story remains intact.

Infrastructure investment continues at scale, manufacturing is receiving renewed policy focus, and production-linked incentives are gradually strengthening industrial competitiveness. Digital public infrastructure has enhanced efficiency, financial inclusion, and transaction formalization, further improving economic productivity.

Additionally, India’s expanding economic diplomacy is reinforcing its long-term growth prospects.

Recent trade and economic engagements with countries such as New Zealand and South Korea reflect India’s broader strategy of diversifying trade partnerships, strengthening supply-chain resilience, and deepening integration with Indo-Pacific economies.

Engagement with South Korea is particularly relevant given complementarities in manufacturing, electronics, semiconductors, clean energy technologies, and industrial investment. Similarly, growing economic cooperation with New Zealand strengthens India’s trade outreach in agriculture, services, education, and strategic regional engagement.

Such agreements are not merely diplomatic exercises—they are part of a wider economic strategy aimed at reducing external vulnerabilities and expanding India’s global commercial footprint.

This is especially important at a time when geopolitical fragmentation is reshaping global trade architecture.

A deeper issue emerging from this ranking episode is the widening gap between perception and economic reality.

India remains among the fastest-growing major economies in the world. Its domestic market scale, demographic profile, infrastructure pipeline, and reform momentum continue to position it favourably in the medium to long term. Yet, headline rankings based solely on nominal GDP can create an impression of decline or stagnation.

This disconnect highlights the limitations of relying excessively on a single indicator to judge economic strength.

Economic influence today is multidimensional. It depends not only on nominal output, but also on productivity growth, domestic market resilience, technological capabilities, external stability, and strategic economic positioning.

Looking ahead, the current ranking dip is unlikely to be permanent.

As exchange-rate pressures moderate and growth momentum continues, India is well-positioned to regain lost ground and strengthen its place in the global economic hierarchy. However, sustaining this trajectory will require continued attention to structural priorities:

• Reducing dependence on imported energy through diversification and domestic capacity expansion

• Strengthening export competitiveness and moving up global value chains

• Deepening trade partnerships and market access agreements

• Enhancing resilience against volatile capital flows and currency shocks

Ultimately, the question is not whether India has fallen behind, but whether we are interpreting global indicators with sufficient analytical nuance.

The movement from fourth to sixth place is not a verdict on India’s economic potential. Rather, it is a reminder that rankings are often shaped as much by exchange rates, commodity prices, and geopolitical volatility as by real economic output.

In conclusion, India’s economic story remains one of resilience, structural transformation, and gradual ascent—even if global metrics occasionally suggest otherwise. The larger challenge is not merely sustaining growth, but ensuring that India’s economic strength is reflected more accurately in international comparisons.

Until then, such ranking movements should be viewed with analytical clarity rather than alarm. Because in today’s global economy, numbers may shift faster than fundamentals.

(Dr. Bhavana Rai, author of this article, is an eminent Economist. Currently, she serves as Joint Director at the FHRAI Centre of Excellence for Research in Tourism and Hospitality (CERTH). She has previously been associated with reputed institutions such as ASSOCHAM, PHD Chamber of Commerce and Industry, and the Institute of Economic Growth)